{kind=link}

Receive free US interest rates updates

We’ll send you a myFT Daily Digest email rounding up the latest US interest rates news every morning.

US bond yields adjusted for inflation have surged to their highest level in 14 years, which has hit technology stocks hard, say analysts and investors.

So-called “real yields” on Treasury bonds have rocketed over the past two weeks as investors have bet that the Federal Reserve can keep inflation under control by keeping interest rates high while avoiding sending the economy into a recession.

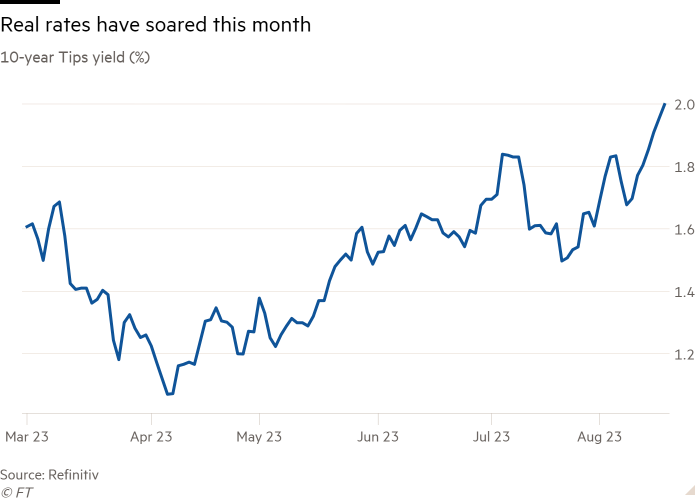

On Thursday the yield on US 10-year inflation-linked government bonds, which are known as Tips, reached 1.998 per cent, its highest level since July 2009, according to Tradeweb data. It has risen 0.4 percentage points in August alone.

At the same time, the 30-year inflation-linked bond reached its highest level since February 2011, while five-year Tips yields hit a 15-year high.

Real yields are inflation-adjusted returns on Treasury bonds, and watched closely by the Fed and investors as a fundamental measure of how much it costs for companies to borrow money, absent the effects of price increases.

Technology stocks offering the promise of high future growth are typically far more attractive to investors when interest rates are low. They can quickly lose their allure when investors are able to obtain higher yields in lower-risk bonds or money market funds. A 4.3 per cent return on a 10-year Treasury note may deter an investor from buying a far riskier asset.

Higher yields can also weigh on the shares of technology companies that rely on debt to finance their growth.

The surge in real yields has dovetailed with a 6.1 per cent decline for the Nasdaq Composite this month, as analysts and traders see real rates hit the sector.

“Higher real rates have led to a stalling-out in the equity rally this year — they have put pressure on equities,” said Gennadiy Goldberg, head of US rate strategy at TD Securities.

“When you see a real increase in borrowing costs, that’s when you see companies starting to make difficult choices,” said Goldberg.

This drop in equities has also been accompanied by a broader tightening in financial conditions — a measure of the cost of and ease with which companies can raise cash.

Financial conditions in the US have loosened since peaking in October, even as the Fed has raised interest rates to the highest level in 22 years. But a Goldman Sachs index of financial conditions has risen in August to its highest level since May.

“Real rates are going up and it is definitely hurting risky assets. It is tightening financial conditions,” said Andrew Brenner, head of international fixed income at NatAlliance Securities.

Treasury yields may have further to rise, and not just because the likelihood of a soft landing is growing.

The US announced earlier this month that it would increase auction sizes of Treasury bonds to bridge the growing gap between tax revenue and government spending. The prospect of more Treasury bonds on the market has helped drive prices lower and yields higher. That change in supply has already sent yields on Treasuries higher.

For the Fed, the real yield will offer an insight into the progress of its monetary tightening campaign, which began last spring.

Real yields did not get much attention when inflation was raging, but now that price pressures are more muted, investors and the Fed are turning to focus more on real yields, said Stuart Kaiser, head of equity trading strategy at Citi.

“Inflation is starting to stabilise, so people focus more on how much has the Fed really tightened,” said Kaiser. “If nominal yields are going to stay at this level even with inflation falling, then you have more restrictive real yields.”

The significant increase in real yields could add to the case that the Fed has raised interest rates sufficiently.

Futures markets are pricing in about a 50/50 chance that the central bank will raises interest rates by an additional quarter-point by November. That may change if economic data continues to show a slowdown in inflation — and if financial conditions remain tight.

“The Fed is increasingly discussing real rates. To me, that is an indication that the Fed believes monetary policy is gaining traction and that they need to think about the next phase,” said Sophia Drossos, an economist at Point72 Asset Management.

“The Fed seems to be considering that the current level of real rates might not be appropriate as the economy decelerates into the next year.”

Additional reporting by Nicholas Megaw in New York