Wrongfooted investors and analysts have been forced to tear up their optimistic predictions of sweeping interest rate cuts this year as rising oil and metals prices add to inflationary pressures, reigniting fears that borrowing costs will have to stay ‘higher for longer’.

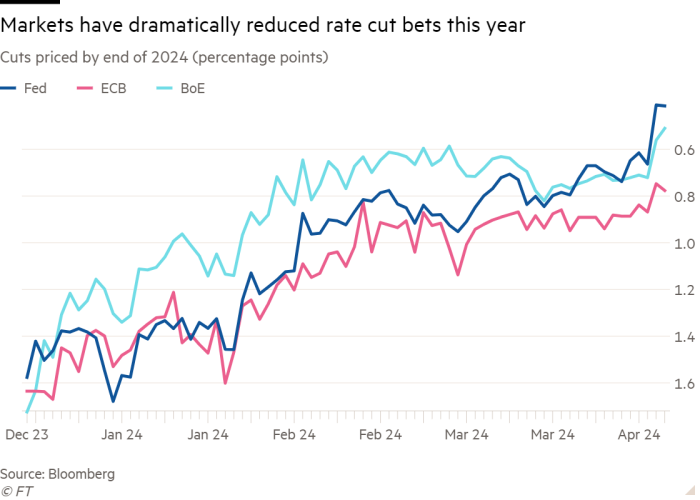

In a dramatic shift in sentiment, markets are now betting that the Federal Reserve will deliver only one or two quarter point interest rate cuts this year.

That compares with the six or more cuts expected back in January and the three that the more conservative Federal Reserve had projected. But after US inflation this week beat forecasts for the third month in a row, traders and fund managers are being forced to look hard at their assumptions.

The rosy forecasts have “just been tossed out the window,” said Greg Peters, co-chief investment officer at PGIM Fixed Income.

“The markets have just been way too optimistic around the prospect for rate cuts,” he added, noting that investors are “behaving a little more rationally now than they were at the beginning of the year”.

The soul-searching stands in stark contrast to December, when the Fed gave its strongest signal yet that it would not raise borrowing costs again and its official so-called “dot plot” projections suggested three quarter-point cuts this year.

That triggered a rally in stocks and bonds and, after investors had been braced for an extended period of elevated borrowing costs that could hurt both assets, prompted talk that the notion of ‘higher for longer’ was finally dead.

But a string of blockbuster jobs data and an acceleration in inflation since then have all but killed off hopes that the Fed and other global central banks will rapidly loosen monetary policy.

“The majority of analysts have been wrongfooted,” said Anthony Todd, chief executive of quantitative hedge fund firm Aspect Capital, referring to expectations of falling inflation and interest rates.

The firm, which manages around $9.4bn in assets and whose main fund is up 21.8 per cent this year, has profited from bets against Treasuries, which have sold off this year as investors have scaled back their bets on rate cuts.

Market pricing for rate cuts this year is now even less than the Fed itself had indicated in December. Some Fed officials have cast doubt on policymakers’ ability to cut rates more than once this year, with Atlanta Fed president Raphael Bostic saying it is even possible rate cuts may have to be moved into next year.

Complicating the outlook on inflation are surging prices for industrial metals and oil — with Brent crude topping $92 a barrel for the first time since October.

The rethink on US rates has also spilled over to European markets, with investors now pricing in three cuts for the European Central Bank and two for the Bank of England in 2024, down from more than six priced for each at the start of the year.

“It is very clear the narrative is changing,” said Torsten Slok, chief economist at investment firm Apollo. “Uncertainty about the narrative of where we’re going in rates is the source of why things are so turbulent at the moment.”

The global economy has also proved more resilient than many had expected, with JPMorgan’s global manufacturing purchasing managers’ index rising into growth territory in January for the first time since 2022, and it continued to grow in February and March.

“I still think the Fed wants to cut once at least this year — but they’re in no rush to do it and they’ll wait for more data to come in to give them more visibility into inflation,” said Ken Shinoda, portfolio manager at DoubleLine.

Despite a rally on Friday as tensions in the Middle East pushed investors into safe assets, expectations for rates to remain high for some time have triggered a global bond sell off, pushing up government borrowing costs on both sides of the Atlantic. Benchmark US and UK government bond yields are up 0.6 percentage points since the start of the year. Equivalent German Bund yields — the benchmark for the eurozone — are up 0.3 percentage points.

However, credit spreads — or the premiums paid by corporate borrowers to issue debt over the US Treasury — are still hovering around multiyear lows, fuelled by intense demand for new bonds and scorching fund inflows.

The average investment-grade US bond spread is now hovering around its tightest, or lowest, level since September 2021, six months before the Fed started raising interest rates. The high-yield, or “junk” spread, widened following the latest CPI release, but is still near its narrowest levels since January 2022, according to Ice BofA data.

For Pgim’s Peters, “a stronger economy with a little inflation isn’t such a bad backdrop for corporate America . . . if you just forget everything else and focus on the fundamentals, I think the fundamental piece is quite good.”

So far the rethink on rates has done little to cool stock markets, with the S&P 500 index of blue-chip stocks up 7.4 per cent this year — helped by the strength of the US economy and excitement about the prospects of artificial intelligence.

But some investors have started to warn that, as the reality of rates staying higher sinks in, stock market exuberance could be running out of steam.

“It feels like we’ve had an easy run up but the landscape is turning more challenging,” said Mark Dowding, chief investment officer at RBC BlueBay Asset Management.

Additional reporting by Laurence Fletcher