{kind=link}

Receive free US Treasury bonds updates

We’ll send you a myFT Daily Digest email rounding up the latest US Treasury bonds news every morning.

The strength of the US economy and the spectre of persistent price pressures have fuelled a big surge in borrowing costs on both sides of the Atlantic as investors rethink the trajectory for global interest rates.

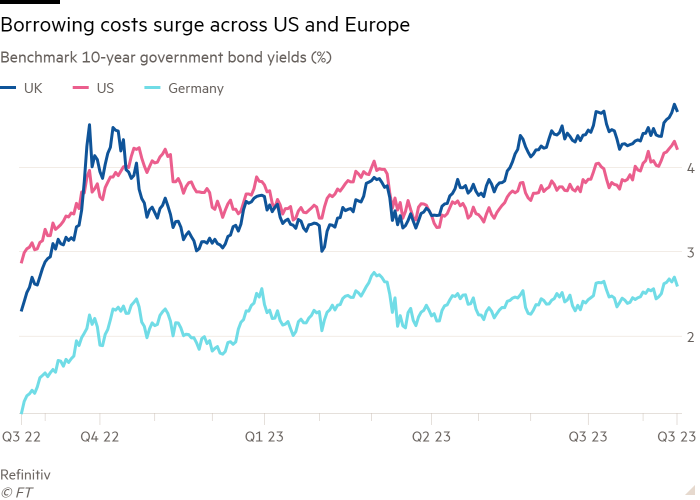

A global bond sell-off pushed benchmark US 10-year Treasury yields close to their highest level since 2007 this week, while equivalent UK gilt yields hit the highest since 2008 and 10-year French government bonds reached levels not seen since 2012.

The rise in yields, which move inversely to prices, comes on the heels of a slew of data that suggests the US economy may be stronger than previously thought and, in turn, inflation may now take longer to moderate. That has prompted investors to push out their expectations for when central banks will be able to start cutting interest rates.

The US Federal Reserve went as far as to warn that there was “significant upside risk to inflation” in its minutes published on Wednesday, even though some officials appeared more sceptical about the need for further rate rises.

The moves have caught out some investors who were getting back into the bond market to lock in the yields on offer, believing that rates had peaked.

“The narrative heading into the summer break was centred around the next big move was for lower rates, but markets seem to be caught wrongfooted here,” said Piet Haines Christiansen, director of fixed-income research at Danske Bank.

“Yields everywhere are going up,” said Andres Sanchez Balcazar, head of global bonds at Pictet Asset Management. “Investors have been selling bonds recently with the view that central banks are not thinking about cuts as the labour market is tight and core inflation is sticky.”

Despite a fall on Friday, yields on benchmark US Treasuries were about 4.23 per cent, 0.27 percentage points higher than at the start of the month. Yields on UK 10-year gilts have risen 0.38 percentage points over the same period while equivalent German Bunds — viewed as a benchmark for Europe — have risen by 0.15 percentage points to 2.62 per cent.

Fuelling the surge in yields is a sharp uptick in government bond supply, said Ed Al-Hussainy, a senior analyst at Columbia Threadneedle. “When you have fundamentals and technicals aligned like you do in this instance, it overpowers everything else.”

The US Treasury department last month announced that it expects to issue a net $1tn worth of bonds in the three months from July to September in order to make up for declining tax revenue.

As issuance has increased, demand from some foreign investors may be waning. US Treasury data shows that the value of Treasuries owned by Japan and China — the two biggest owners of US debt — fell by 11 per cent and 12 per cent, respectively, over the year to June.

James Athey, an investment director at Abrdn, noted that the move from Japan last month to relax its yield curve control policy “may well encourage Japanese investors to reduce their global holdings in favour of domestic bonds”, which could continue to put upward pressure on yields of US and European debt.

Investors also say that, with many traders away on holiday, lower trading volumes this month are causing oversized moves in bond prices.

“It’s crazy volatile at the moment because liquidity is pretty rubbish,” said Mike Riddell, a bond portfolio manager at Allianz Global Investors. “Most US data has surprised to the upside over the past six weeks and this has had an outsize effect on bond prices.”

US retail sales data this week was significantly more buoyant than expected, rising 0.7 per cent in July, while the Philadelphia Fed’s manufacturing business outlook survey for August surged to its highest level since April 2022.

“With growth set to print around 2 per cent for the third quarter in a row, it is not clear why inflationary pressure should dissipate,” said economists at Citigroup.

It may take “sustained higher 10-year yields to slow the economy and the housing sector in particular to reattain 2 per cent target inflation”, they warned.

While US core inflation — which strips out volatile food and energy prices — has cooled in recent months to 4.7 per cent, it remains far above the Fed’s target. The UK is still grappling with persistently sticky price pressures, with core inflation at 6.8 per cent, while in the eurozone the rate is 5.5 per cent. Higher commodity prices across the continent have helped pushed up inflation expectations to decade highs.

Labour markets also remain tight, with average hourly earnings in the US increasing by 4.4 per cent year over year in July. In the UK, official figures this week showed annual pay growth of 7.3 per cent, the highest growth on record.

“You are seeing wage pressures everywhere and they put pressure on employers to charge higher prices — it’s just not conducive with a quick drop back to target inflation,” said Robert Tipp, head of global bonds for PGIM Fixed Income.

He expects to see a “stable centre of gravity for long-term yields at 4 per cent” over the next one to three years. “The market perception at the moment is that the neutral Fed fund rate is 2.5 per cent and the Fed will eventually return to it, but I really question that,” he said.

Central banks on both sides of the Atlantic have insisted that they will remain data dependent on future interest rate decisions.

Economists at Evercore said the recent surge in yields “represents a serious tightening of financial conditions”, which in turn may aid in the Fed’s efforts to tame inflationary pressures. They concluded that it would help to “offset the upside surprise to growth with respect to the outlook for inflation”.

Traders are now betting that the fed funds rate will to stay close to the current target rate of 5.25-5.5 per cent until the middle of next year, that the European Central Bank will deliver one more 0.25-percentage-point rise by the end of the year to 4 per cent and that the Bank of England’s rate will peak at 6 per cent by early next year.