Another year means another round of trying to answer the market’s favourite question: Who, exactly, is going to buy all these Treasuries?

Goldman Sachs predicts the US will issue a record $1.4tn of coupon-bearing notes and bonds this year, on net. That’s up from $391bn last year.

Is this reason to fret about fiscal folly? Nope, not really. We’re not writing “bUt WhO’s GoNnA PaY FoR iT?” stories just yet, and for good reason.

First of all, the US will end up issuing a smaller amount of net debt than last year, however, when its debt outstanding rose by $2.4tn. (That wave of supply growth was driven largely by bills, which pay yield not through coupons but by selling at a discount and redemption at par.)

What’s more, the amount of coupon-bearing Treasuries the private sector will need to absorb will see a smaller jump, rising to $1.85tn from $1tn, according to GS’s estimates. This is because the Federal Reserve will almost certainly start slowing its balance-sheet shrinkage, or QT. Last year, the Fed’s QT efforts required private investors to buy a whole bunch of supply that had been previously purchased by the Fed. In other words, while the net amount of coupon-bearing Treasury issuance didn’t rise much, the amount hitting the market did.

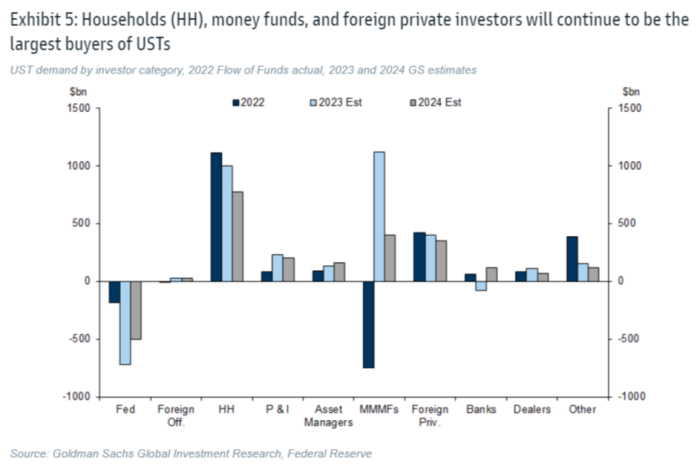

There is still interest in who, exactly, is going to buy all of this supply of coupon-bearing Treasuries. Diamond-handed sovereign forex reserves and liability-matching pensions? Or mutual funds and/or hedgies who might prefer to trade actively across markets? While somebody is always going to buy US debt, the question is cost: Basically, the stakes are the volatility of mortgage rates.

To get a sense of who’ll be buying, GS strategists look at recent flow of funds and auction data, aiming to game out future sources of demand.

They predict that so-called “households” will lead the charge — thanks to an entertaining quirk in the data, that includes levered hedge funds and practitioners of the much-discussed basis trade:

GS explains:

We expect a continued increase in [levered funds’] positions will be needed to clear the markets at current spread levels, though purchases from these holders will likely drop from their recent elevated pace to a still-high pace of ~$770bn. Other domestic holders, likely state and local governments and corporate Treasuries, will also likely participate, albeit at a significantly slower pace of purchases. Demand for these other categories is also likely to be focused on shorter maturities.

In other words, like the premium (and inherent leverage) in Treasury futures could continue to prop up a pillar of demand for the cash market. This isn’t necessarily a bad thing for market stability. It could be, if lots of levered funds doing the trading are generalists and will bail in favour of a fire sale in another market. On the other hand, levered funds have the benefit of not being crucial intermediaries of lots of real-world economic activity the way banks are. ¯\_(ツ)_/¯

Anyway, money-market funds should be a large source of demand as well this year, says GS, albeit a somewhat smaller one than in 2023. They were massive buyers of bills last year, as investors piled into the asset class to take advantage of high short-term rates. From GS:

In 2024, we expect MMF will buy a smaller, but still sizable $400bn, partly on account of a stalling (or potential decline) in AUM growth, and diminishing RRP facility balances that these funds may be readily willing to substitute out of. These funds likely bought over $1tn of T-bills last year, and appear to have reduced their holdings of shorter maturity coupon securities and FRNs by about $75bn. That latter change could reverse this year, given the reduced bill supply relative to demand.

Foreign private-sector investors also provided an “unexpectedly strong bid” last year. The hedgie / levered-fund bid is probably playing a small role there too, though:

This strong demand can partially be attributed to the fact that these investors likely bought over $89bn of T-bills, for which an inverted curve is less of an issue. Additionally, some of this demand, such as purchases in the Caribbean (~$42bn) or countries with large resident custodial banks (in Europe), could reflect hedge fund activity (and accumulation of basis positions; more below). Accounting for these factors, we project foreign private investors will purchase a still healthy $350bn of USTs this year, whereas the foreign official sector purchases will likely total less than $50bn.

Fed rate cuts could also draw more plain-vanilla asset managers into the mix:

Mutual funds, closed end funds, and ETFs, which we collectively refer to as “asset managers,” could double their purchases, buying about $160bn this year on account of the start of Fed easing.

Commercial banks could also become a net buyer of Treasuries this year. As the Fed prepares to cut rates (er, eventually) and slow its deposit-draining QT efforts, banks may be somewhat less eager to reduce their Treasury exposure. And the ultra-short-dated assets banks bought after duration became a powder keg last year will mature, and that cash will need to be reinvested if loan growth doesn’t pick up. GS doesn’t expect banks to become major bidders for duration, however:

We anticipate commercial banks will go from net selling last year to net buying this year. Much like asset managers, the onset of Fed easing is likely to “crowd in” some investment from those buyers. In addition to potential declines in funding rates, there are a few additional considerations that could aid this transition. First, a clearer timeline for the end of the Fed’s QT program should offer banks greater clarity on the evolution of their deposit bases. Second, given the shorter maturities of assets in banks’ liquidity portfolios, many lower yielding securities are likely to be maturing over the course of the year, and banks will need to replace them unless loan growth proves to be exceptionally strong. We expect demand from banks will be mostly focused on shorter maturities.

Pensions and insurers will be a solid base of demand as well.

Large private pensions’ funded ratios have jumped above 100 per cent in the past few years thanks to higher interest rates; that companies will try to offload them onto insurers’ balance sheets, and/or match their benefits and liabilities in the Treasury market. Public pensions are, to put it gently, not as well-funded. But they’ve still been buying plenty of Treasuries, and GS expects that trend to continue:

. . . we expect continued sizable purchases from pensions and insurers. Intermediate-to-longer maturity USTs should see about $150bn demand from a combination of private and public (state and local) pension plans . . . When looking at this ratio on a disaggregated basis, we expect another 15-20% of private plans will move to a sufficiently high funded status to increase de-risking or risk transfer activity that supports demand for duration. Milliman’s public pensions study estimates a lower aggregate funded ratio of about 76% at the end of last year, with only 7% of plans exceeding fully funded status. Nevertheless, flow of funds data suggests that these retirement funds bought $69bn of USTs in the first three quarters of last year.

Given our expectation for a strong performance of financial assets, boosted by robust economic growth and likely Fed easing, we expect further improvement in funded status, and continued purchases from this group as well. Finally, we project that these funds, combined with insurers, are likely to purchase around $50bn of shorter maturity USTs.

To step back, what does all of this mean for market depth and liquidity? Well, it isn’t going to reduce the premium in futures markets, the strategists say, which should further entrench the reasons for trading the so-called Treasury basis.

So . . . long live the basis trade?!