Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

In the darkest moments, even the tiniest shard of light can provide solace. Enter the UK asset management sector, likely to provide a flicker of optimism this week with interest rates no longer rising and restructuring efforts moving apace. Do not get carried away: this is an industry facing deep structural challenges.

The basic issue remains that revenues are flatlining. Money is moving either to cheaper passive funds or to specialist and alternatives funds that promise juicier returns. Traditional active managers are squeezed in the middle. There is huge pressure on fees. Fee compression of 15 per cent in the five years to 2022 equates to $55bn of forsaken revenues based on that year’s AUM, consultancy BCG calculates.

This is a fragmented sector, and one facing increasing regulatory burdens. While these outfits invest globally, persistent outflows from UK-focused funds does not help the mood — or more domestic-focused groups such as Liontrust.

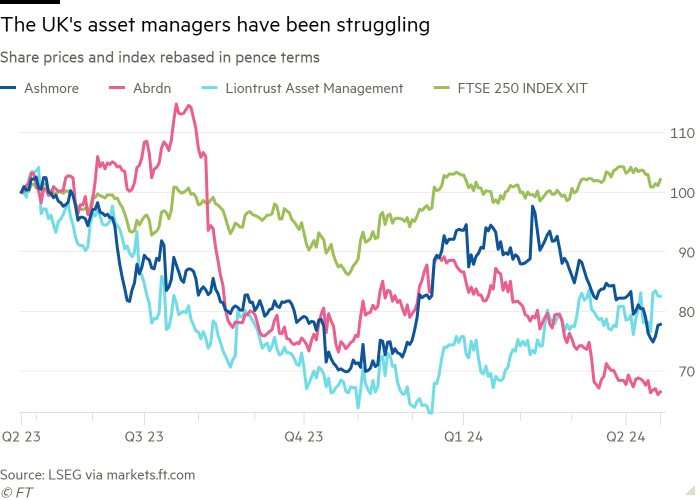

Then there are specifics. Clients pulled a net $2bn from emerging markets-focused Ashmore in the first quarter. After all, why invest in risky far-flung places when you can make bigger and surer bets in the US and Europe? Bold calls, such as on Chinese real estate and Lebanese sovereign debt, have proved contrarian for the wrong reasons. Performance deters new money: 44 per cent of AUM have underperformed over three years and 38 per cent over five years. The $1.1bn total return fund has underperformed over three, five and 10 years.

Abrdn, which reports on Wednesday, illustrates the perils of lacking scale when paired with hefty overheads: a cost/income ratio of 94 per cent on £366.7bn of AUM at its investment business resulted in a nugatory £50mn of operating profit last year.

Both these asset managers, as well as many of their smaller peers, have underperformed the FTSE 250 in the past year, and put industry bosses into turnaround mode. Ruffer is just the latest to lay off staff; Abrdn kicked off the year by announcing 500 job cuts as part of efforts to help save £150mn. It has also acquired online platforms, including Interactive Investor, and sold subscale businesses.

The end result should be more consolidation. But in a people business, this is no easy task. Look at the 2017 coupling that created Abrdn or Liontrust’s kiboshed acquisition of Swiss rival GAM. Talks over the sale of Natixis Investment Managers continue to drag on. It will take more than a shifting macro backdrop to turn these shops around.