Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

New year messages from managers do not often set hearts singing. Universal Music chief executive Lucian Grainge’s annual memo to staff is an exception. His musings are closely read by equity analysts as they can set the tone for industry-wide changes.

At the turn of 2023, the head of the world’s largest record company called for a new royalties model for streaming, to combat the rise of what he referred to as “noise”. His 2024 memo suggests the industry is not finished battling threats such as fraud and generative artificial intelligence.

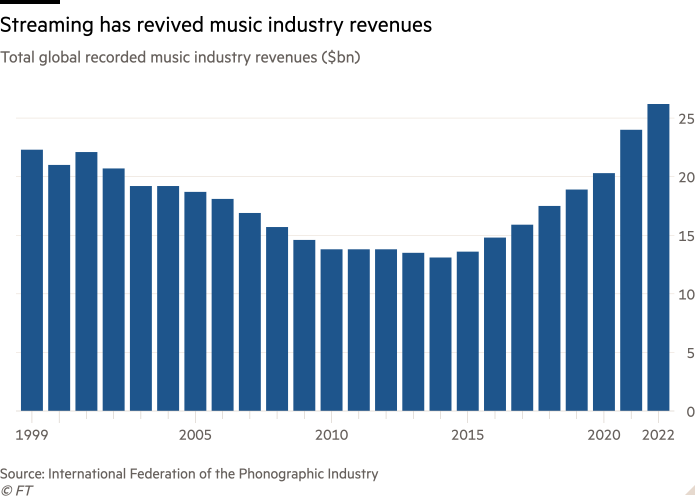

Music is a prime example of a sector that has faced repeated disruption in the past quarter of a century — and has so far managed to survive near existential threats.

Last year, Grainge followed through on his resolutions. In September, Universal struck a deal with French music streaming service Deezer that marked the first major change in streaming royalties since the advent of the industry in the late noughties.

Streaming platforms such as Spotify, which launched in 2008, helped to revive an industry that had, from the late 1990s onwards, struggled against illegal file-sharing and downloads.

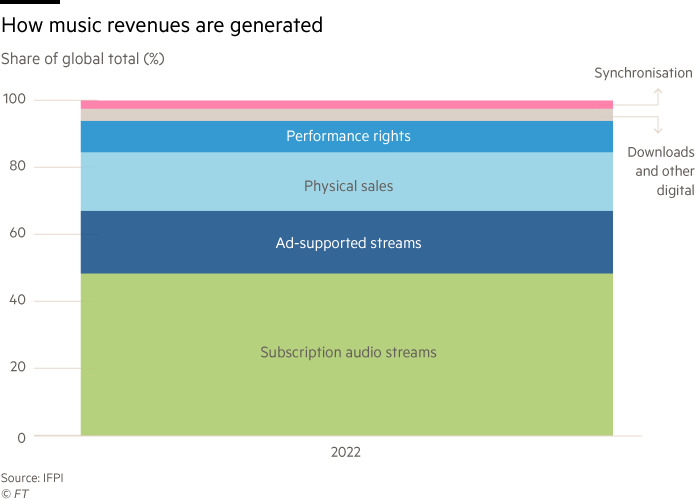

Streaming drove global recorded music industry revenues to double between 2014 and 2022. Yet the royalties model had not evolved in the past 15 years, despite the emergence of new threats. The ability for almost anyone to create and stream content led to a surge in uploads, which is only expected to accelerate with the proliferation of generative AI. This threatened to dilute professional artists’ — and music labels’ — share of royalties paid.

Under Universal’s agreement with Deezer, professional artists who generate larger numbers of streams are remunerated better than creators of other content, including computer-generated sounds. Rival Warner Music also later signed up to the Deezer model in France.

Grainge’s 2024 memo suggests other platforms may soon follow what he has coined an “artist-centric” approach. A separate agreement between Universal and Spotify struck last year has similar principles.

Such an approach is, of course, also label-centric. It is in Universal’s interests for the model to become systemic. Industry-wide revenue growth from streaming has slowed in recent years. Universal’s subscriptions and streaming revenue is forecast to rise 7.5 per cent to €5.72bn for 2023, according to analyst estimates on Visible Alpha. It had racked up growth of 19 and 17 per cent respectively in 2022 and 2021.

Shares in Universal fell 11 per cent in the first half of 2023 as investors fretted over the consequences of generative AI, including the rise of “deepfake” songs that mimic the voices of professional artists. However, price rises and the Deezer agreement have since helped push the shares up more than 30 per cent.

Other factors should help growth. Citi’s Thomas Singlehurst points to price rises: platforms including Spotify and YouTube lifted costs for listeners in 2023, but the effects should still be felt this year.

Universal struck an agreement announced in October to start distributing vinyl and CDs from artists signed to rival BMG, although it is expected to be a low-margin activity. Grainge has promised “efficiencies”, or job cuts. This, Singlehurst believes, should help keep margins “at least stable” in 2024.

Other innovations are needed to stay ahead of disruption. Grainge hinted that Universal is looking at how it can monetise the relationship between artists and their closest followers with “superfan experiences”. It is easy to imagine dedicated fans paying for exclusive content.

The music industry’s battle against AI and fake content is only at the start. But investors can at least gain confidence that Universal is on the offensive.

Activist interest suggests the UK has a management problem

The UK’s persistently undervalued stock market is irresistible to global activist shareholders. Campaigns rose across Europe last year, according to data from consultants at Alvarez & Marsal. The UK was the most popular location for the seventh year running.

This is a dubious distinction, given concerns about the UK’s equity market malaise and longstanding underperformance. But the agitators appear to have had some success. Two years after an activist shareholder campaign, according to the data, UK company share prices beat the wider market by 9.2 per cent. Campaigns in the US and Europe generated lower outperformance of 6 per cent on average.

The UK’s appeal to activist investors makes sense. Not only does it have more listed companies than other European markets but share registers are more open. Larger free floats help in two ways. There are fewer large influential owners, including families or founders, who wield influence over the company. A more distributed shareholder register can also mean a more willing investor audience to coalesce behind activists’ demands.

But the market may also simply be ripe for their intervention. A&M’s analysis suggests activist campaigns focused only on dealmaking, governance or environmental and social factors reap lower rewards than those that home in on operational performance. Bumpitrage efforts — where shorter-term activism can boost takeover offers — yielded positive results at deals for tobacco group Swedish Match and UK software group Aveva.

The UK market trades at roughly a one-third valuation discount to global stocks. There is much debate about whether sector composition, growth outlook, income-focused investors or waning domestic pension money is the root cause.

The repercussions, however, are clear given the rise in private equity-backed takeovers and a growing roster of companies, such as Tui, CRH and Ferguson, opting to move their listing overseas. The A&M findings add weight to the optimists’ case that UK stocks trade at lower multiples because they offer lower returns. Once adjusted for this, the discounts often disappear.

Lex is the FT’s concise daily investment column. Expert writers in four global financial centres provide informed, timely opinions on capital trends and big businesses. Click to explore