{kind=link}

Receive free US Treasury bonds updates

We’ll send you a myFT Daily Digest email rounding up the latest US Treasury bonds news every morning.

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. After a few months of risk-on, the market’s feeling nervy again. The S&P 500 is off 3 per cent from its recent peak, as investors sweat the timid price reaction to earnings beats. Tech is looking the shakiest. With long yields rising, Microsoft is down 11 per cent from mid-July and Nvidia is off 14 per cent. More on the latter below. Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

Nvidia 2023 = Cisco 2000?

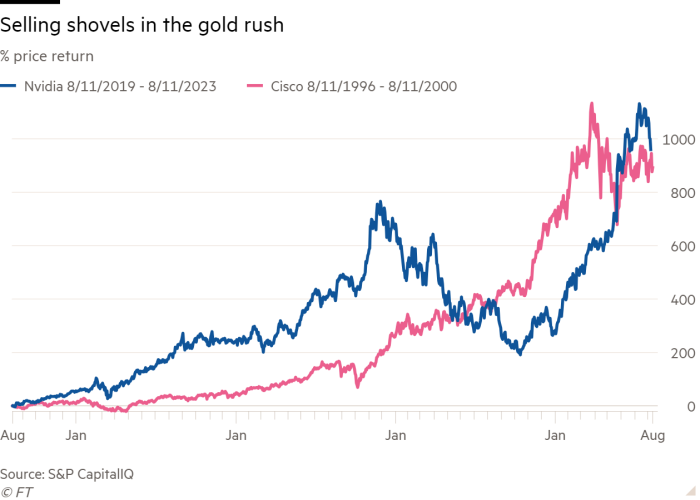

Here is a chart which I have carefully designed to make as scary as possible:

That is the percentage price appreciation of Nvidia over the past four years, lined up against the share price appreciation of Cisco in the four years leading up to August 11 2000. The reason the chart is scary is not simply because of the dizzying ascent of the two tech companies. It is scary because the stories driving the two stocks at the two time periods depicted are remarkably similar. Cisco was pitched as the crucial infrastructure provider for the internet revolution — whatever the internet became, we were told at the end of the last century, it would use Cisco switches and routers to become it. Nvidia is pitched as the crucial infrastructure provider for the artificial intelligence revolution — whatever AI becomes, we are told, it will use Nvidia chips to become it.

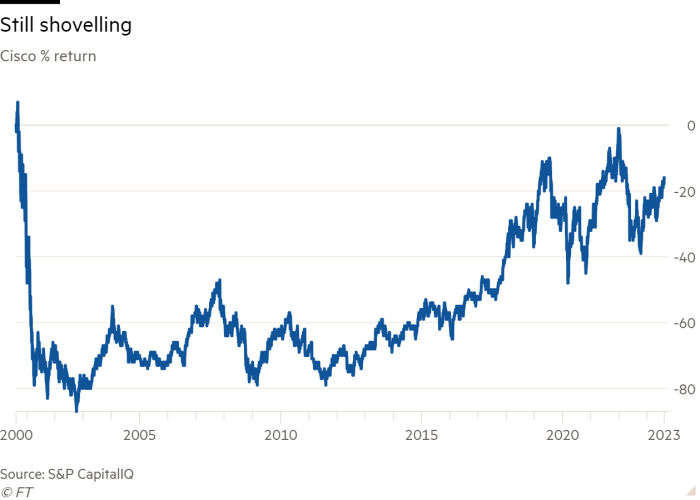

What makes this similarity unsettling is the price return of Cisco since August of 2000:

The stock has gone from $64 to $54 over the intervening 23 years; include dividends, and investors are just about breaking even. It’s been a horrible couple of decades, and the crucial point about its horribleness is that Cisco’s underlying results over the period have been very good. Cisco earnings per share have grown at a compound annual rate of just under 10 per cent since 2000. But the stock was so expensive at the outset that the growth couldn’t save it.

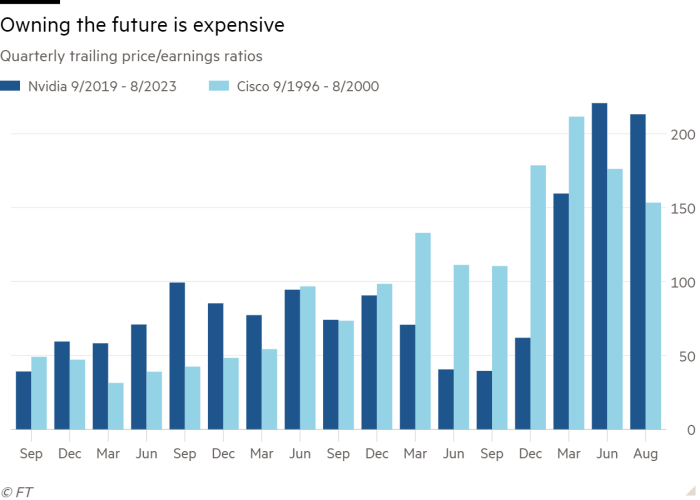

How expensive was Cisco? Here are the trailing PE ratios of the two companies over the same periods depicted in the first chart:

I could have picked a different time period to make the run-up in Cisco’s and/or Nvidia’s stock price more or less extreme. But the trailing P/E ratios are what they are, and Nvidia is even more expensive than Cisco was in 2000 on this metric.

Nvidia’s management suggests that investors should use a non-GAAP calculation of earnings per share, and Wall Street analysts obediently do so. On Nvidia’s calculation, the stock looks less expensive — 133 times trailing earnings rather than 212 times, a bit cheaper than Cisco was. But non-GAAP earnings at Nvidia exclude share compensation and merger-related costs, which should absolutely never and almost never, respectively, be excluded from earnings. GAAP is clearly the better metric.

That said, earnings are expected to shoot up in the current fiscal year at Nvidia, to almost $8 a share from $3.43 last year, on a non-GAAP basis. So reverse the spurious non-GAAP adjustments, and assume that Nvidia earns $6.50 on a GAAP basis this year. Then the chipmaker would be at 60 times earnings or so, much cheaper than Cisco was in 2000 (though hardly a bargain!).

It’s not that simple, though. Is the current fiscal year an exceptionally good one, a cyclical peak or near-peak in earnings? Or is it instead a new plateau of earnings Nvidia will only build upon? On the one hand, the chip industry is cyclical and hyper-competitive; on the other, Nvidia by all accounts has a big technological lead on its peers. I have no opinion on this, but the market is betting heavily that this year is just the beginning. The Wall Street consensus is for Nvidia to make $19 a share in GAAP terms in 2028.

What if bonds are no longer the safe asset?

Bonds were slammed in 2022, but the worst is behind us. After a one-time valuation reset from uber-low rates, bonds are returning to form as the “safe” asset class. As inflation comes down, the punchy yields available on 10-year Treasuries look attractive. Investors would do well to lock them in now.

This thinking is common enough, represented across the financial press as well as in this column. Is it wrong? Over the weekend, two sharp financial writers, the FT’s John Plender and the WSJ’s Spencer Jakab, published pieces arguing bonds’ risks are due for a rethink. They join a growing number making some form of this case, notably including Charles Goodhart’s demography-focused argument and Nouriel Roubini’s doomsday prophecies.

Between them, Plender and Jakab highlight four risks to bonds, which we have distilled:

-

The bond bull market is over. In Unhedged last month, Jenn Hughes wrote about the five long-term shifts in rates since the mid-19th century. One appears to have just ended. The tailwind of bond capital appreciation from 40 years of falling rates is gone:

-

An environment where inflation and rates are higher and more volatile will destroy bonds’ short-term volatility-dampening benefits.

-

In the longer term, higher inflation and a scary US fiscal outlook raises the spectre of outright negative real returns.

-

The 2022 episode illustrated that bond-stock correlation can shoot up at painful times. This calls into question bonds’ biggest long-term upside, the ability in a downturn to rebalance bond-market gains towards beat-up stocks.

There is plenty here one could object to, but take it at face value for a moment. Leaving aside edge cases such as insurers and pensions funds, if Plender is right that bonds are “unsafe and very risky”, what then?

First and foremost, cash looks better. Jakab quotes Ray Dalio: “Cash used to be trashy. Cash is pretty attractive now. It’s attractive in relation to bonds. It’s actually attractive in relation to stocks.” A six-month bill currently yields 5.5 per cent, well above the 4-ish per cent available on a long bond and without any equity risk. You also get some optionality value. If stocks fall from their lofty valuations, a handy funding source is at your disposal. In a higher-inflation, rising-rate environment, similar rebalancing out of bonds to stocks risks realising paper losses on the bonds. In other words, holding bonds to maturity has an opportunity cost.

Bonds are still a different asset class from stocks, likely with some diversification benefit to holding both. But if bonds have lost their safe, boring status to a volatile-inflation world — that is, if real returns aren’t guaranteed, even when held to maturity — the investment approach must change. A bond investor may need a stockpicker’s discipline and risk management.

Of course, it’s a different story if fears of higher-for-longer inflation are overdone. Bond bulls such as JPMorgan’s David Kelly tend to think the economy will gently return to 2 per cent inflation by next year. With inflation dislodged, rates can return to neutral, which the Fed reckons is about 2.5 per cent. Falling rates would cut the yield on cash, leaving the bond investors who locked in 4-plus per cent yields feeling pretty good. It would also give bond investors some meaningful capital appreciation.

There is much more to say here, and we’d be interested to hear what you think. (Ethan Wu)

One good read

How the waste stream of finance works.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.