Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

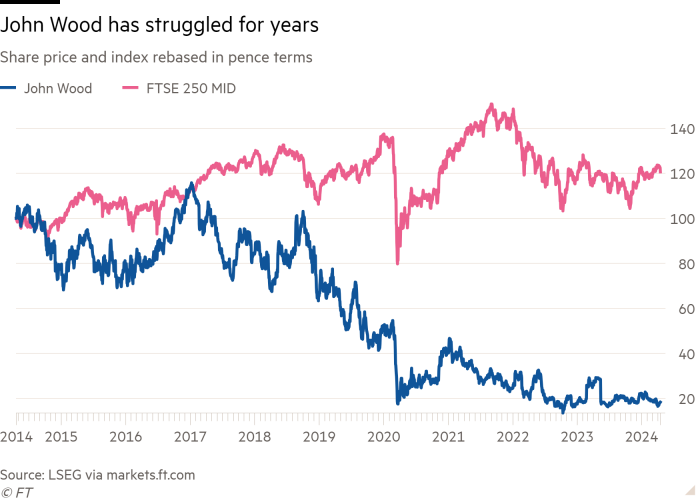

When a UK company’s share price goes south, simply blame the London market.

Increasingly, companies or their investors are pointing to weak trading liquidity, or a supposed yawning valuation gap, compared with US peers for poor stock performance. The London market is not in the best shape. But it also cannot be the scapegoat for all UK corporate woes.

Activist investor Sparta Capital Management is calling on London-listed engineer Wood Group to consider a US listing to address the “continued underperformance of its shares”. It references the “recent successful attempts by corporates to move their primary listing away from markets which . . . do not recognise the true worth of their businesses”.

This is delusional. Wood is no CRH or Flutter. It is a small FTSE 250 engineer that is midway through yet another turnaround after its calamitous £2.2bn takeover of Amec Foster Wheeler in 2017, which saddled it with debt and legal liabilities. Its problems are of its own making. It is not obvious why US investors would be any more willing to buy shares until the company shows it can generate sustainable positive free cash flow.

You cannot blame Sparta for agitating. Wood’s stock languishes around 142p — a painful 41 per cent below the final takeover price offered by Apollo a year ago before the private equity group got cold feet. Frankly, 240p a share for Wood looked high then. At some point between 240p and Apollo’s opening gambit of 200p, a deal should have been done.

But a New York listing would do little to solve Wood’s woes. Given its £971mn market value, it is not clear what US index it would get into.

All efforts must be directed at trying to repair Wood’s damaged reputation, after years of overpromising and underdelivering. It has a new chief executive in the form of the well-respected Ken Gilmartin. But investors have long memories, argues Jefferies analyst Mark Wilson. And its latest turnaround effort comes with a $50mn cash impact that will delay hitting positive organic free cash flow by a year, to 2025. In 2023, this was -$265mn, an improvement on -$704mn the prior year.

You can imagine the excitement on Wall Street as this mid-cap, cash sinkhole turns up. Sparta, which also wants a review to look at a sale, might fare better with bidders. But there is little reason to think a deal will be struck now, after last year’s interest faltered.

The London market has its difficulties. But false narratives are an unhelpful distraction in trying to address them.

Lex is the FT’s concise daily investment column. Expert writers in four global financial centres provide informed, timely opinions on capital trends and big businesses. Click to explore