Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

A surge in the number of Americans choosing “buy now, pay later” payment methods for their holiday shopping is raising concerns among advocacy groups that many lower-income consumers will find themselves struggling to pay their bills in the new year.

Usage of the modern-day layaway plan — in which payments are typically made in instalments with no interest except to the merchant — has hit an all-time high this holiday season. BNPL contributed to $10.1bn of online spending since the start of November, up 17 per cent from the same period of 2022, Adobe Analytics calculated.

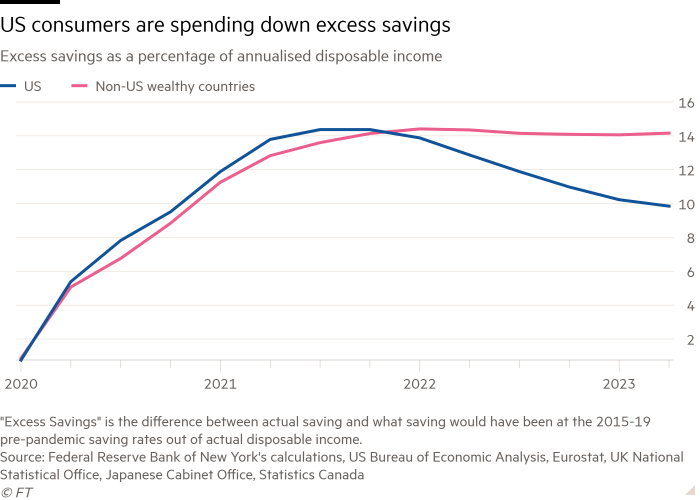

The payment methods are gaining in popularity as US household savings fall below levels recorded before they were boosted by government stimulus during the Covid-19 pandemic. Consumer sentiment has sunk to a six-month low.

The effects of two years of above-normal inflation have also driven up prices for shoppers. Deferring payment is one way for consumers to cope with the strain.

“We are in an environment where things cost more, so it’s somewhat predictable that consumers can get into situations that can quickly spiral into unaffordable debt burdens,” said Delicia Reynolds Hand, director of financial fairness advocacy at Consumer Reports, a research group.

While BNPL gained traction in Europe and Australia about a decade ago, it took off in the US during the pandemic. Between 2019-21, volumes of such loans increased almost tenfold, according to the Consumer Financial Protection Bureau.

Researchers at the Federal Reserve Bank of New York warned in a September report of “the potential risks of overextension, whereby frequent use of BNPL funding leads to excessive debt accumulation over time”.

A 2023 academic study showed that consumers spent 20 per cent more with BNPL than they would otherwise have done. Ecommerce group Shopify, which has enjoyed record-setting holiday sales this year, encourages vendors to use BNPL to drive higher sales.

Many BNPL companies have been moving away from zero-interest payment models to interest-bearing instalment loans in recent months, said Reynolds Hand. “The cost to the consumer is likely to have increased,” she said.

One of the leading BNPL companies, Affirm, told investors that 74 per cent of their gross merchandise volume in the latest quarter consisted of interest-bearing loans. More than 90 per cent of those loans offered up to a maximum annual percentage rate of 36 per cent, Michael Linford, chief of finance, said in a shareholder letter.

“Because we do not charge late fees or other hidden charges, our success is aligned with consumers successfully managing their finances and responsibly extending access to credit,” Affirm told the Financial Times. Affirm has said the BNPL industry would benefit from more regulation.

But some BNPL lenders also charge late fees, often about $7 per missed payment on an average loan size of $135, according to the CFPB.

One source of concern is that BNPL funding is not subject to the same reporting requirements as credit cards or other forms of credit, so the extent of an individual’s BNPL use across different vendors is not clear.

“There could be major stacking of loans going on because the BNPL [loans] are not being reported,” said Armen Meyer, co-founder of the American Fintech Council trade group and former head of regulatory strategy and public policy at LendingClub.

Americans’ credit card debts hit $1.08tn in the third quarter, up $154bn year-on-year and the largest jump since 1999, according to the New York Fed. A CFPB survey in March found that 88 per cent of BNPL users also had an open credit card.

“BNPL borrowers were, on average, much more likely to be highly indebted, revolve on their credit cards, have delinquencies in traditional credit products, and use high-interest financial services,” the report concluded.

This article has been amended to correct the share of Affirm’s gross merchandise volume that consisted of interest-bearing loans