Goldman Sachs this week celebrated 25 years as a public company. The Wall Street investment bank has not always wanted to act like one.

In the early years after the initial public offering, longtime chief financial officer David Viniar was said to privately joke that “disclosing the weather is too much information”.

Goldman’s IPO in May 1999 was a seminal moment for the then 130-year-old investment bank, and its 221-strong partnership, which had already spent almost 15 years debating whether to seek public equity capital.

The firm plans to mark the occasion by assembling a replica of the New York Stock exchange balcony where then-chief executive Hank Paulson rang the opening bell, so employees can take their own picture.

“The need for permanent capital made it inevitable we would go public,” said Lloyd Blankfein, the second of just three chief executives of the bank since its IPO, and a partner before the float.

“We feared we would lose our distinctive partner culture that had propelled our success. Miraculously, that culture has largely survived, and still affects how people conduct themselves and meet their responsibilities,” Blankfein told the Financial Times. “And the title still has cachet on the Street.”

But being a partner in Goldman Sachs in 2024 no longer means what it once did.

In the quarter of a century since the bank called time on its partnership structure and handed ownership of one of New York’s most prestigious financial institutions to stock market investors, Goldman’s bankers have sometimes struggled with the shift in accountability to outside shareholders.

In addition to Viniar’s private joking, chief executives Paulson and Blankfein would not speak on earnings calls, while the bank did not set regular public financial targets.

“The disclosures of Goldman after it became public would be laughable if it wasn’t so awful for investors,” said Mike Mayo, research analyst at Wells Fargo who has tracked Goldman’s stock for around two decades.

Insiders said Goldman’s level of disclosure at the time was not particularly bad compared with peers such as Bear Stearns or Lehman Brothers, both of which failed in the financial crisis.

Still, “their disclosures lagged peers for a while, many years even after the IPO”, said Jason Goldberg, a research analyst at Barclays who has covered Goldman for more than 10 years.

The bank’s early success meant that it could afford to be more opaque. It wooed potential IPO investors in glitzy hotels including the Ritz. “That just shows the aspirational multiple they were looking for,” recalls one investor.

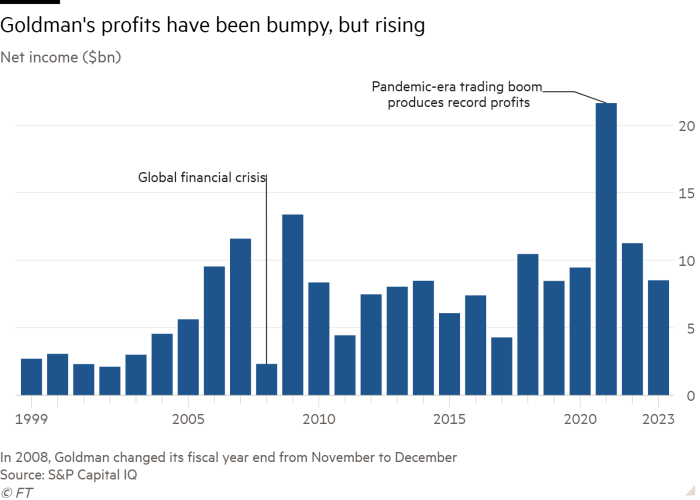

For its first decade as a public company, it handed investors swashbuckling profits from its money-spinning investment banking and trading businesses. Profits tripled between 2000 to 2007. It is alone among the big six US banks in outperforming the S&P 500 over the past 25 years.

“When things are good, you get away with a lot more,” said Goldberg.

In the early years after its float, Wall Street analysts struggled to understand how the bank made its money. “It wasn’t until John Waldron [bank president since 2018] that I actually had . . . a good meeting at Goldman Sachs,” said Mayo.

“Very nice and smart people, don’t get me wrong. David Viniar is a star CFO. He just wouldn’t answer questions in meetings. He’d talk and then at the end, like what did we get out of that? I don’t think we got anything out of it. I think that was their goal.”

The start of its second decade as a public company, in the depths of the 2008 global financial crisis, paled in comparison to the first — and opened it up to a far harsher regulatory spotlight as it switched from a brokerage firm to a bank holding company.

When David Solomon became chief executive in 2018, his “mandate was to make Goldman function more as a public company even though it had been public already for two decades”, said Mayo.

Solomon has tried to make the bank more shareholder-friendly, hosting the company’s first investor day four years ago and speaking on quarterly results calls. “They’ve now made strides under Solomon’s tenure,” Goldberg added.

Still, if analysts now understand how Goldman makes its money, in recent years it is the bank that has grappled with how best to generate it for investors.

Following the 2008 financial crisis, the bank wound down its proprietary trading arm. For several years, Goldman kept wagering its own capital on investments such as private equity and real estate. It is now in the process of paring back that business to make its earnings less volatile.

Instead, it has sought more predictable earnings elsewhere.

A foray into consumer lending, with the launch of its Marcus brand in 2016 and the subsequent $1.7bn purchase of online lender GreenSky, later written down, proved an expensive misjudgement. The bank is now emphasising its growth in asset and wealth management franchise: a move its longtime rival Morgan Stanley made more than a decade ago.

Goldman makes money today largely as it did before its IPO: from investment banking, trading and managing money for the wealthy.

It also managed its own IPO in the way it has managed countless others for clients in the years since. It priced the shares astutely, towards the top of its target range, but sufficiently low to allow a pop of more than 30 per cent on the first day of trading on the New York Stock Exchange on May 4.

“After years of telling clients to leave an opportunity for the stock to rise in the pricing, we had to show we had priced it responsibly,” said Dan Dees, who as a young investment banker worked on Goldman’s IPO and now co-runs its banking and markets division.

Another person familiar with the roadshow said Paulson had made clear that the deal could never trade below its IPO price. “Lehman, Morgan Stanley, Bear [Stearns] were all waiting to say these guys couldn’t even do their own IPO,” the person said.

In other ways the firm — and Wall Street — have changed far more fundamentally over the past 25 years. Of the 13 underwriters on its equity offering, only three — Morgan Stanley, JPMorgan and Goldman itself, which led the float — have avoided being subsumed into other financial institutions.

“Look at how many of our competitors don’t exist anymore,” said Goldman partner Tim Ingrassia, one of only six current Goldman employees who was a partner at the time of the IPO.

The firm still bestows the title of partner on its 400-odd most senior employees, with a new class made up every two years. But even after 25 years, only 19 per cent of its partners are women — up from 6 per cent at the time of the IPO.

The float handed a windfall to the class of pre-IPO partners that not even Solomon, who joined the bank months after Goldman listed, can rival.

Solomon told the FT that his predecessors Paulson, Jon Corzine “and the partners at the time made the right decision”.

“You have to evolve and grow, but the remarkable thing is how they set us up to retain our partnership culture,” Solomon said. “We worked very hard to ensure that being a partner here is aspirational and that partners continue to contribute to our culture of excellence.”

But for selling the bank, the pre-IPO partners received just under 265mn shares, worth about $14bn in total or $63mn for the average partner. Paulson’s stake was worth $219mn at the IPO price, while the shares of Corzine were worth more than $230mn.

“The result was there were partners that were worth more than they ever expected,” said one Goldman banker who worked at the firm during the IPO. Goldman’s stock has since risen around eightfold. The $14bn of shares would be worth about $113bn today.

By comparison, Solomon’s shares in Goldman are worth about $66mn.

Perks for new partners today include special access to funds managed by Goldman, a guaranteed salary of $1mn, plus a bonus, an annual private gathering, and funds to donate to charity through the bank’s philanthropic arm.

The IPO bred a dynamic of “haves and have nots” between the partners who had benefited from the public share sale and the more junior employees who had no equity interest in the firm, according to people who worked at Goldman at about that time.

Part of the work by Paulson was to reward younger employees who were top performers. Another ex-Goldman employee said: “There was a clear emphasis from [Paulson] to make sure the organisation benefited from the talent that was there that had not benefited from the windfall of the IPO.”

Paulson told the FT: “Goldman Sachs needed to grow significantly to meet the needs of our investing and corporate clients — the elephant was becoming too big for the partnership tent. We were solving for size and capital, and we needed to do so in a way that maintained our culture.

“We created a partnership structure within the public company and broadly shared the economic benefits across the firm,” said the man who served as chief executive for seven years before he left to become US Treasury secretary.

“It went seamlessly. In the ensuing years, we increased our position as the leading investment bank in the US, Europe and Asia, and we did so while maintaining a one-firm, teamwork culture.”

Goldman’s trio of chief executives as a public company

Hank Paulson

Henry “Hank” Paulson started at Goldman in 1974 having worked in Washington at the Department of Defense and in the Nixon administration. An investment banker, he was early in pushing Goldman into growing its presence in China. He was appointed co-CEO alongside Jon Corzine in 1998 but the partnership was short lived — Corzine left Goldman within the year, leaving Paulson alone at the helm when Goldman completed its IPO in 1999. Paulson left Goldman in 2006 to become Treasury secretary under George W Bush.

Lloyd Blankfein

Lloyd Blankfein entered Wall Street with the commodities trading business J Aron, which Goldman bought. He became a partner in 1988 and president in 2003, emerging as Paulson’s heir apparent. Barely a year after he was anointed chief executive in 2006, Blankfein had to steer the bank through the mortgage market crisis, where Goldman was accused of profiting from the turmoil through a “big short”. He won credit internally for defending Goldman from public criticism but Blankfein’s bet that the trading business would bounce back failed to materialise during his tenure, which ended in 2018.

David Solomon

After stints at Drexel Burnham and Bear Stearns, Solomon joined Goldman in 1999 as a partner — narrowly missing out on the IPO — to help run the firm’s leveraged finance business. He later co-ran investment banking before becoming co-president in 2017 alongside Harvey Schwartz in what was viewed as a two-way battle to succeed Blankfein. Solomon won in 2018 and set about making Goldman a more shareholder-friendly company with more durable earnings. However, his misjudged push into consumer lending and high-profile DJ-ing appearances have been controversial inside the bank.

Goldman’s life as a public company

1999

Goldman floats on the NYSE, raising $3.7bn and valuing the investment bank at about $30bn. It now has a market capitalisation of $141bn

2000

The bank buys Spear, Leeds & Kellogg, one of the most powerful trading companies on the NYSE floor, for $6.5bn. Goldman subsequently wrote down its value and cut staff

2006

Lloyd Blankfein replaces Hank Paulson as chief executive

2008

Goldman becomes a bank holding company in the depths of the financial crisis

Two days later, Warren Buffett invested $5bn in the bank, bolstering its capital and liquidity and paving the way for a further equity capital raise by Goldman

2013

Goldman Sachs Asset Management acquired Deutsche Asset & Wealth Management for an undisclosed sum

2015

Goldman bought $16bn of deposits from GE Capital, picking up an additional source of funding as General Electric unwound its finance arm in the wake of the financial crisis

2016

Goldman launches Marcus, its attempt to move into retail banking

2018

David Solomon replaces Lloyd Blankfein as chief executive

2019

Goldman celebrates its 150th anniversary

2020

Solomon hosts Goldman’s first-ever investor day, part of a shift to be more shareholder-friendly

2021

Goldman announces two deals: the acquisitions of Dutch asset manager NN Investment Partners for €1.6bn and GreenSky, an online lender, for $2.2bn, as it looked to build its presence in consumer lending.

Goldman reaps record profits from an investment banking and trading boom during the pandemic

2022

Goldman retreats from consumer lending after racking up billions in losses

2023

Solomon lays out plans to build up Goldman’s asset and wealth management business at another investor day

The bank sells GreenSky after two years at a steep loss, part of its move away from the retail banking business

2024

Goldman’s shares reach an all-time high

Additional reporting by Mari Novik