Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

In any other sector, a market share of more than 50 per cent might lead to complacency. In the relatively young US sports betting industry, there is no time for self satisfaction.

Disney’s ESPN was just one potentially formidable competitor that entered the market last year to challenge leaders Flutter — owner of FanDuel — and DraftKings. Early signs suggest Flutter can still flourish stateside despite the competitive assault.

Since the US Supreme Court in 2018 struck down a federal law banning sports wagering, the US market has been seen as a new source of rapid growth, particularly for international betting companies that faced tighter regulation in mature markets such as the UK.

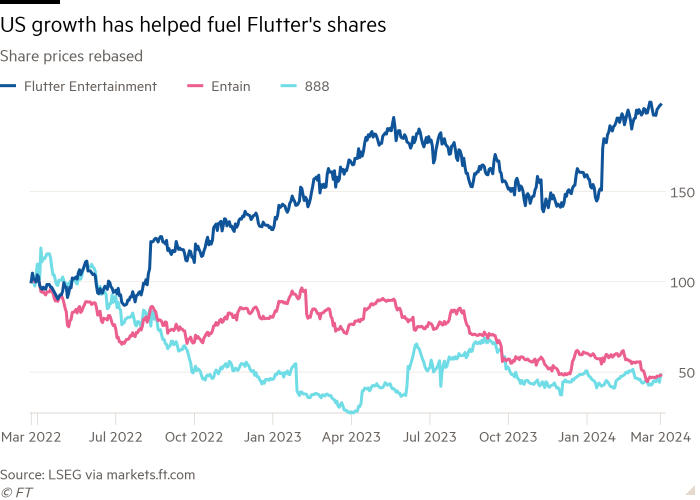

Flutter — previously Paddy Power Betfair — was an early mover. It now operates mobile sports betting in 22 states and online gaming in five. Its US business delivered its first full year of profitability last year. Further growth is expected: US adjusted earnings are forecast to more than triple to about $710mn in 2024 on revenues of $5.8bn to $6.2bn, up from $4.4bn in the US last year.

Performance so far this year suggests Flutter’s confidence is not misplaced. Total US revenues were up nearly 56 per cent between January 1 and March 17. At the end of 2023, its share of the sports betting market stood at 53.4 per cent.

Of course, much can still change. Despite Flutter touting its superior technology, competitors are quick to copy once a new product proves successful, points out Peel Hunt’s Ivor Jones.

Yet the adage that size matters does seem to still hold true stateside, where margins are thin and competition to acquire new customers fierce. Smaller, highly leveraged peer 888 Holdings is looking at options to sell or exit its US consumer business as part of its latest turnaround strategy, which includes a slightly desperate rebrand to evoke.

Flutter’s US growth prospects, plus its secondary listing in New York in January, have allowed it to far outpace challenged London-listed rivals. Its shares have gained more than 20 per cent in the past 12 months. Shareholders will vote on switching its primary listing to New York in May.

On a forward price/earnings ratio of 35 times, Flutter’s shares look expensive. But its strong US business justifies the premium compared with UK peers. With gearing coming down, Flutter also has the bandwidth to make acquisitions to defend its position in the US if necessary.

New US competitors will not find it easy to gain territory from the market leader.