Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

BHP has turned its pickaxe to the equity markets to find the metal it desires: copper.

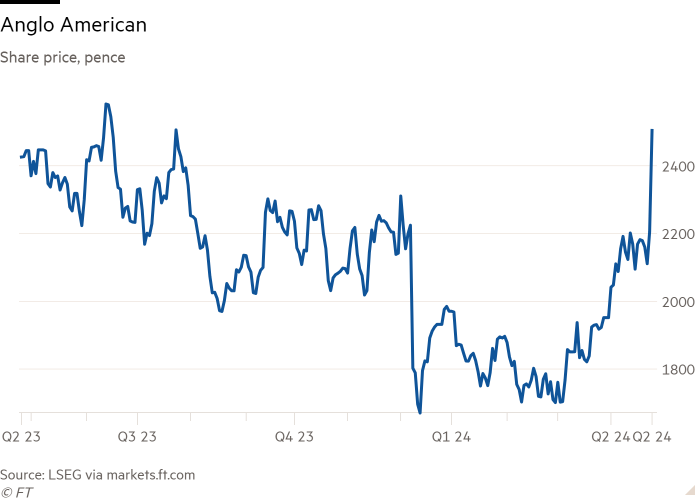

Anglo American, one of the few miners to build a copper mine in recent years, offers growth in the red metal, buried amid its South African iron ore and platinum assets. BHP’s complex all-share approach worth £25.08 per Anglo share values Anglo’s equity at £31.1bn. That price isn’t enough to extract a deal.

There are other obstacles to this tie-up. The deal will require not just Anglo shareholder approval but that of South Africa’s government. Competition law there has a public interest clause that could slow or block any deal approval.

Anglo American’s South Africa exposures, with about a fifth of its assets there, explain much of its persistent enterprise valuation discount to peers. Its 5 times multiple of forward ebitda, before BHP’s approach, was about 15 per cent below BHP and Glencore, and 40 per cent under US-listed Freeport-McMoRan.

BHP, which has always gone out of its way to avoid emerging market risk, will pitch this as an opportunity for South Africa. Anglo holds a substantial stake in its Johannesburg-listed subsidiaries in the country: its dividends from those businesses, Anglo American Platinum (Amplats) and Kumba Iron Ore, are largely invested outside the country.

BHP proposes handing to Anglo’s shareholders the miner’s stakes in Amplats and Kumba. Some of that cash flow could stay in South Africa, runs the argument, creating jobs there. That logic is debatable. Local shareholders still require dividends. And Anglo investors who want direct exposure presumably already own what they need.

Combining the shares in Amplats and Kumba with a slug of BHP stock means a price about 32 per cent above Anglo’s average share price over three months.

That doesn’t look enough. Anglo’s shares have been slowly recovering after a warning about production late last year. At £25.08 a share, the deal is pitched only 19 per cent above where Anglo was trading earlier this week. That headline price and premium are already down slightly, thanks to Amplats and Kumba shares falling on Thursday.

Cost savings could be another issue. Besides getting copper tonnes on the cheap, it is not clear what the benefits would be to BHP. The two companies could perhaps share infrastructure for their metallurgical coal mines in Queensland Australia. Both have iron pellet businesses in Brazil. Cost savings from copper look unlikely, except perhaps from marketing 40 per cent more copper production.

The combined group would get 46 per cent of forward ebitda from iron ore and 44 per cent from copper, points out Jefferies. To up the price, BHP would need to find some savings there. The miner will need to dig deeper to get this project over the line.